March 2024 San Francisco Market News

Quick Take:

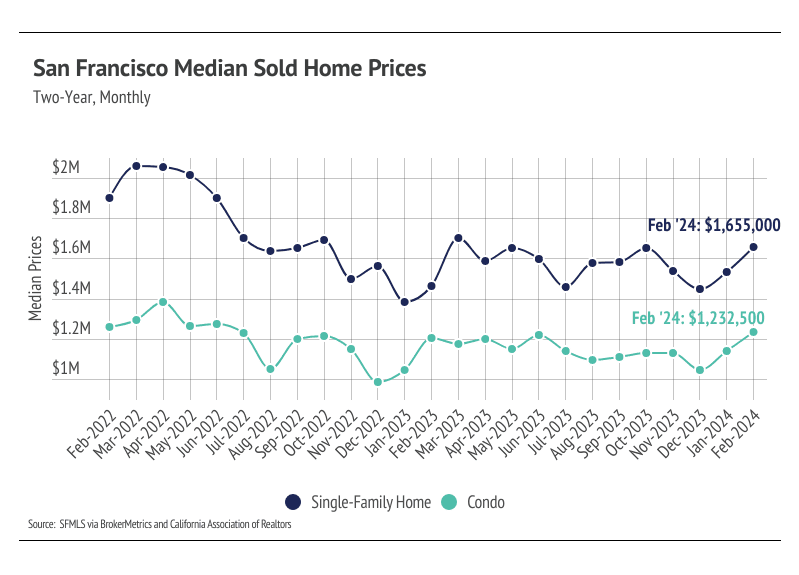

Note: You can find the charts & graphs for the Big Story at the end of the following section.

Quick Take:

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

Stay up to date on the latest real estate trends.

Quick Take: Mortgage rates have ticked up slightly over the course of the past year, and coincidentally, so has the median sale price of a home in the US. According t… Read more

Quick Take: Mortgage rates have ticked up slightly over the course of the past year, and coincidentally, so has the median sale price of a home in the US. According t… Read more

Quick Take: Affordability remains a concern across the country despite lower interest rates compared to this time last year. New homes are being added to the market, … Read more

Quick Take: Home prices declined modestly in Q4 2024, showing atypical price stability in the second half of the year. Because prices didn’t contract significantly in… Read more

Quick Take: Home prices declined modestly in Q4 2024, showing atypical price stability in the second half of the year. Because prices didn’t contract significantly in… Read more

Quick Take: Elevated mortgage rates dominated the housing market in 2024, and 2025 may look similar if inflation starts to ramp up again. Corporations are already inc… Read more

Any questions at all, happy to help!